Indonesia poised for more rapid domestic growth in 2013, driven by low-cost carriers

15th March, 2013

| inShare |

© CAPA

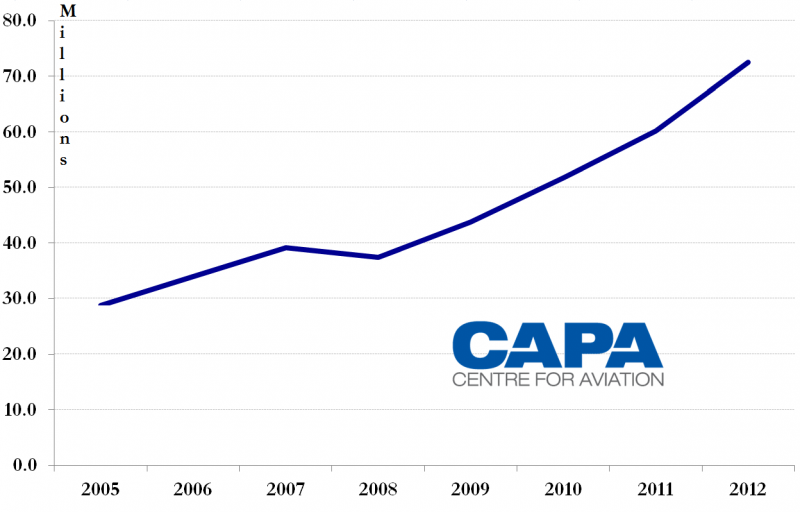

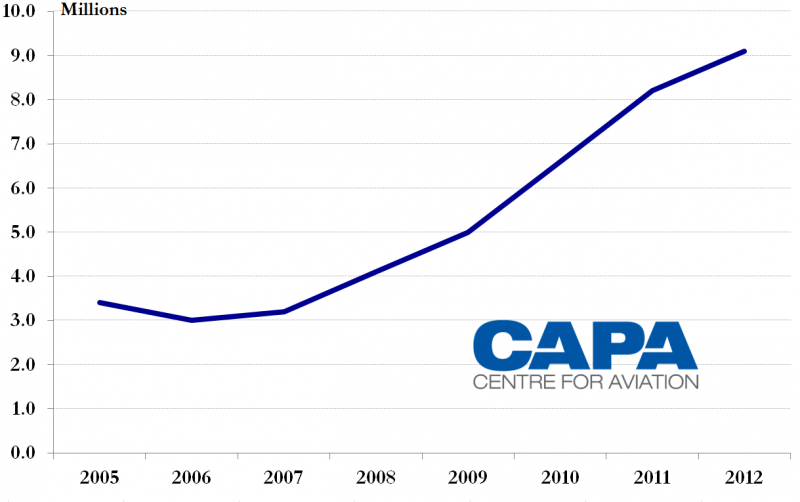

The Indonesian domestic market is poised for more rapid growth in 2013 despite the bankruptcy and suspension of operations at Batavia, which had been Indonesia’s fourth largest carrier. The void left by Batavia has been quickly filled by other carriers, primarily Tiger Airways affiliate Mandala and Garuda Indonesiasubsidiary Citilink. Nearly all of the country’s other remaining carriers are also pursuing rapid expansion in 2013. Indonesia’s domestic market grew by 20% in 2012 from 60.2 million to 72.5 million passengers, according to preliminary data from Indonesia’s DGAC. This makes Indonesia the fifth largest domestic market in the world (after the US, China, Japan and Brazil) and one of the fastest growing. The 20% increase in domestic passenger traffic for 2012 follows 16% growth in 2011, 18% growth in 2010 and 17% growth in 2009. As a result Indonesia’s domestic market has nearly doubled in only four years – from 37.4 million passengers in 2008.

While the exit of Batavia will likely result in slower growth compared to the last three years, more double-digit growth is likely in 2013 given the rapid capacity and fleet expansion from the remaining carriers. Indonesia annual domestic traffic (millions of passengers carried): 2005 to 2012  Note: 2012 figure is preliminary Source: CAPA - Centre for Aviation; Indonesia’s DGAC and INACA The 72.5 million passenger figure for 2012, provided to CAPA by Indonesian airline association INACA, should be finalised within the next couple of months. At that point the DGAC will also provide a carrier-by-carrier breakdown.

Note: 2012 figure is preliminary Source: CAPA - Centre for Aviation; Indonesia’s DGAC and INACA The 72.5 million passenger figure for 2012, provided to CAPA by Indonesian airline association INACA, should be finalised within the next couple of months. At that point the DGAC will also provide a carrier-by-carrier breakdown. Garuda Group grows its share of the domestic market

Only one Indonesian airline group, Garuda, is publicly traded and reports traffic data although two other carriers, Indonesia AirAsia and Mandala, are owned partially by publicly traded companies outside Indonesia. Garuda in Feb-2013 reported mainline domestic traffic of 14 million passengers for 2012, an increase of 14% compared to 2011. Garuda also reported domestic traffic for its fast-growing budget subsidiary Citilink of 2.9 million passengers, an increase of 76% compared to 2011. Based on the DGAC total figure of 72.5 million, Garuda as a group captured a 23.2% share of Indonesia’s domestic market in 2012. (This is not necessarily a completely accurate figure as Garuda and the DGAC have slightly different ways of measuring domestic passengers. For example, the DGAC reported for 2011 Garuda Group domestic traffic of 13.7 million passengers, giving it a 22.8% share, while Garuda itself reported for 2011 domestic traffic of 13.9 million passengers, which would equate to a 23% share). Garuda’s current strategy, which was implemented about two years ago, focuses on winning back market share from Lion by accelerating growth at Citilink. The Citilink operation in 2011 only carried 1.6 million passengers with a fleet of less than 10 aircraft. Citilink aims to carry 10 million passengers in 2013 and 19 million passengers in 2015. Citilink’s fleet is expected to grow from just over 20 aircraft currently to 75 aircraft by the end of 2015. This includes 50 A320s and a new fleet of 25 ATR 72 turboprops, the first batch of which will be placed into service in 4Q2013 and used to compete against Lion regional subsidiary Wings Air on short island-hopping routes. Citilink transitioned in Jul-2012 from a unit of Garuda using Garuda’s operating certificate to a fully owned subsidiary with its own AOC. Citilink is expected to eventually seek an initial public offering and expand into the international market but for now its focus is on closing the gap with Lion domestically. See related article: Citilink regional expansion will further intensify competition between Garuda Indonesia and Lion AirLion’s position as Indonesian domestic market leader is assured

Based on 2011 data from Indonesia’s DGAC, Lion was the leading domestic carrier with 25 million passengers and a 41.5% share. When also including Wings, the Lion Group transported 27 million passengers in 2011 for a 44.8% share. The Lion Group likely saw its share of the market increase further in 2012 as it added domestic capacity at a clip exceeding 30%. According toInnovata data, Lion’s ASKs were up 35% in Dec-2012 compared to Dec-2011, making it the fastest growing airline among the world’s top 50. See related article: United ends 2012 as world’s biggest airline, Emirates third. Turkish and Lion the biggest movers Lion is predominately a domestic carrier, with 91% of its ASKs and 96% of its seats currently allocated to the domestic market. According to Innovata and CAPA data, Lion currently offers about 820,000 domestic seas, a 41% increase over Mar-2012 levels. Wings provides another 133,000 weekly seats, which is roughly double the capacity it provided a year ago. Privately-owned Lion does not report traffic or financial figures. Lion’s ambitious owner and CEO, Rusdi Kirana, has said the group aims to capture 60% of Indonesia’s domestic market by 2017. But such a goal seems unrealistic given the pace of expansion of its competitors and the overall market. Lion could potentially see its share reach 50% in 2013 as it benefits, along with Indonesia’s smaller LCCs, from the exit of Batavia. Lion is also launching in 2013 a new full-service subsidiary in Batik Air. Batik will allow Lion to play at the top end of Indonesia’s domestic market, which is dominated by Garuda and is also growing, albeit more slowly than the budget end of the market.Lion-branded operation to see slower growth in 2013

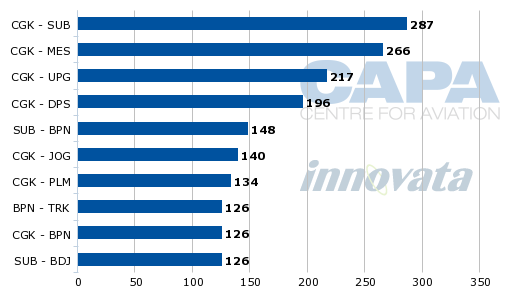

But the launch of Batik and a new joint venture hybrid carrier in Malaysia, Malindo, means Lion will likely slow down capacity expansion at the main Lion brand in 2013. Malindo is expected to launch services by the end of Mar-2013 with two 737-900ERs and have a fleet of 12 aircraft by the end of 2013. Batik is expected to launch later in 2013, potentially as early as May-2013, and operate a fleet of at least six 737-900ERs by the end of the year. As Lion has been taking delivery of additional 737s at a rate of two per month or 24 annually, only six additional aircraft are expected to be added at the Lion-branded operation in 2013. Lion also has been working towards phasing out its 737 Classics which means the total size of the fleet at the main Lion brand could be flat in 2013. Lion currently operates 82 737NGs and nine 737 Classics, according to CAPA data. The group has 330 additional 737s on order. Wings currently operates 22 ATR 72s with another 38 of the type on order, according to CAPA data. Wings’ rate of expansion is expected to continue to be much faster than Lion albeit at a smaller base as Wings is taking new ATR 72s at a rate of about one per month. But the carrier is also in the process of phasing out its small fleet of Dash 8s and DC-9s. The Lion Group could potentially accelerate expansion of its fleet or push back the launch of Batik if it decides it needs to pursue faster growth at the Lion-branded operation in response to intensifying LCC competition. Faster growth would be tempting as otherwise the Lion brand risks losing market share to the country’s smaller LCCs – Citilink, Indonesia AirAsia and Mandala. Lion is not as well positioned to fill the void of Batavia as its three LCC competitors because it already has the most extensive domestic network in Indonesia by a wide margin and offers the most frequencies on trunk routes. With most of Lion’s additional capacity already allocated to Malindo and Batik, Lion also lacked the aircraft to respond to Batavia’s grounding by adding capacity on routes which had been served by Batavia. Lion Air top 10 domestic routes ranked on weekly frequencies: 11-Mar-2013 to 17-Mar-2013 Source: CAPA – Centre for Aviation & Innovata Lion is generally considered the price leader on trunk routes. Its low cost structure, use of large narrowbody aircraft with over 213 seats and big size, which gives Lion economy of scales that others cannot match, allows it to be aggressive with fares. Lion’s low fares are generally matched by the other LCCs and in some cases by the full-service carriers. But its competitors generally struggle to make a profit as their costs are higher. Batavia was not considered a budget carrier but it operated aircraft in single-class configuration and generally matched the fares of Lion and other LCCs.

Source: CAPA – Centre for Aviation & Innovata Lion is generally considered the price leader on trunk routes. Its low cost structure, use of large narrowbody aircraft with over 213 seats and big size, which gives Lion economy of scales that others cannot match, allows it to be aggressive with fares. Lion’s low fares are generally matched by the other LCCs and in some cases by the full-service carriers. But its competitors generally struggle to make a profit as their costs are higher. Batavia was not considered a budget carrier but it operated aircraft in single-class configuration and generally matched the fares of Lion and other LCCs. Citilink, Mandala and Express Air assume risks in taking over Batavia routes and slots

Batavia captured 11% of the domestic market in 2011, down from 14% in 2010. While 2012 data for Batavia is not yet available, the carrier saw its market share slip in 2012 as it cut capacity – particularly in the second half of the year as it ran into financial problems and had to return a large portion of its fleet. When it suspended services on 31-Jan-2013, Batavia accounted for less than 5% of domestic capacity, according to Innovata data. Three carriers responded in the immediate aftermath of Batavia’s suspension by offering to take over the grounded carrier’s routes – Citilink, Mandala and small little known full-service carrier Express Air. These carriers offered, in discussions with the Indonesian Transport Ministry, to assume some of Batavia’s routes and passengers. In exchange for traffic rights and slots, the carriers were required to fly, at no charge, Batavia passengers that had already paid for future travel on those routes. Offering to take over the Batavia routes is bit of a gamble as it is costly and technically the reallocation of slots and traffic rights is only temporary. Batavia theoretically could resume operations and take back its slots and traffic rights. This is unlikely to occur as Batavia’s owners prefer to liquidate rather than restructure, but if creditors push for a restructuring rather than liquidation, new owners could potentially be secured and the airline could re-launch. For example, Mandala was able to re-launch services in Apr-2012, ending a 15 month period of suspended operations while restructuring and securing new owners while under bankruptcy court supervision. But Mandala ended up losing its slots at Jakarta to the dismay of its new owners, which initially thought the slots could be re-secured. Given the lack of transparency in slot distribution and redistribution in Indonesia it is unclear what would happen if Batavia re-launched. Citilink, Mandala and Express Air are essentially betting that the ex-Batavia slots and traffic rights secured will become permanent. Slots have become a valuable commodity in Jakarta as there are no additional slots available at peak periods. The lack of slots at Jakarta has particularly posed a roadblock for Mandala, which after re-launching services had to initially schedule almost all its Jakarta flights to takeoff very early in the morning (in some cases before 05:00) and not return to base until late at night. This limitation prevented the carrier from offering multiple frequencies on its Jakarta routes and increased costs as Mandala was forced to rest its crews at other stations, which is highly unusual for a short-haul LCC.Batavia bankruptcy creates opening for Mandala

Mandala pounced when Batavia decided on 30-Jan-2013 to suspend operations and was the first carrier to make an offer to the Indonesian transport ministry to take over Batavia's routes and passengers. Mandala immediately took over from Batavia rights and accompanying slots for Jakarta to Padang, Surabaya, Pekanbaru and Singapore. About a month later it also took over Batavia’s traffic rights and accompanying slots for Jakarta to Pontianak. For Jakarta-Pekanbaru, Mandala quickly moved up its launch date for the route and added flights. Mandala was already planning to launch Jakarta-Pekanbaru on 14-Feb-2013 with one daily flight using an early morning departure slot of 05:20. As CAPA previously reported, Mandala moved up the launch by two weeks following Batavia’s bankruptcy. It briefly operated three daily frequencies to carry stranded Batavia passengers and now offers two daily frequencies, including the original early morning departure and an additional departure in the afternoon, a schedule it plans to maintain. See related article: Mandala, Indonesia AirAsia and Citilink to benefit most from Batavia bankruptcy Jakarta-Surabaya is a route Mandala had already launched on 04-Jan-2013, about four weeks prior to Batavia’s suspension, with one daily flight. Taking over the route gave Mandala access to Batavia’s Jakarta-Surabaya slots and traffic rights. But Mandala has not yet added capacity on the route. Mandala launched Jakarta-Padang on 01-Dec-2012 with one daily flight. It currently operates two daily flights on the route, using an ex-Batavia slot. But Mandala will revert to just one daily flight on the route with a 05:35 takeoff from Jakarta (its original flight) from 31-Mar-2013, according to the Tiger booking engine. Mandala has not yet launched Jakarta-Singapore. But as CAPA reported previously, the carrier is planning to launch four daily flights on the route sometime during the northern hemisphere summer 2013 season. This uses traffic rights made available from Batavia’s bankruptcy as well as the subsequent expansion of the Indonesia-Singapore bilateral. See related article: Jakarta-Singapore route poised for big capacity increase, led by Tiger and Mandala When Mandala does launch flights on Jakarta-Singapore, Mandala will be required to carry Batavia passengers that were previously ticketed for future travel at no charge. The ticketed passengers do not necessarily need to travel on the same dates for which they had purchased their tickets. For Jakarta-Pontianak, Mandala is operating one daily flight from 15-Mar-2013 to 30-Mar-2013, according to the Tiger reservation system. Mandala has a notice on its website offering Batavia’s Jakarta-Pontianak passengers free flights on these dates. Mandala is currently not selling Jakarta-Pontianak for travel after 30-Mar-2013. It could later resume the service once it takes delivery of more aircraft or could decided to shift the slots it has received for Jakarta-Pontianak to other new routes.Airlines taking over Batavia slots can re-use them for other routes

Taking over the rights from Batavia does not mean the new carrier has to be operating the route already and it does not require the new carrier to launch services immediately. The only requirement essentially is for the new carrier to transport Batavia’s ticketed passengers on the route. The new carrier also doesn’t have to use the slots Batavia previously used for the same route. In some cases the slots can be reallocated to other routes as long as the new carrier meets the requirement of flying Batavia’s passengers. Given the value of peak hour slots at Jakarta, it is not surprising that the former Batavia routes, which have been taken over by Mandala, Citilink and Express Air, were the routes that Batavia operated at peak hours. Several of Batavia’s routes have not yet been taken over as the slots they come with are not valuable.Citilink and tiny Express Air see opportunity to expand in Jakarta

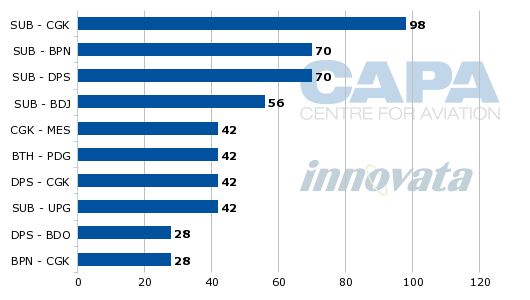

Citilink has taken over 14 routes while Express Air has taken over two routes. As in the case with Mandala not all of these routes have yet been launched and in some cases they were already served by the carrier. Express Air is a small carrier based in Makassar and operating six 737s along with a small number of regional aircraft, according to CAPA data. Express Air transported only 316,000 domestic passengers in 2011 according to Indonesian DGAC data, making it the 10th largest carrier with a 0.5% share of the market. Taking over Batavia routes allows the carrier to expand in Jakarta and secure slots it otherwise would struggle to obtain. Express Air has ambitions of becoming a more significant player by acquiring 737NGs and expanding into the international market. But Indonesia is a highly competitive market that is challenging for new or smaller carriers that try to expand beyond regional niche roles. Citilink is a much bigger carrier and was already planning to rapidly expand its network in 2013. The Batavia bankruptcy provided opportunities to re-prioritise and add capacity in certain markets, particularly at congested Jakarta. Citilink’s largest base is currently Surabaya, where it offers about 61,000 weekly seats while in Jakarta it currently offers about 50,000 weekly seats, according to Innovata data. Jakarta-Surabaya is Citilink's largest route while its second, third and fourth largest routes link Surabaya rather than Jakarta with other destinations. Lion, however, has nearly three times as many frequencies on Jakarta-Surabaya. Citilink top 10 domestic routes ranked on weekly frequencies: 11-Mar-2013 to 17-Mar-2013 Source: CAPA – Centre for Aviation & Innovata

Source: CAPA – Centre for Aviation & Innovata Mandala fleet to reach 12 aircraft by 4Q2013

Citilink and Mandala were able to respond quickly following Batavia’s bankruptcy as they had spare capacity. Mandala had just taken delivery of its seventh A320 but was not yet operating a seven-aircraft schedule. Mandala has opportunities to continue adding flights on former Batavia routes as it plans to grow its fleet to 12 aircraft by the end of the year. Mandala plans to take its eighth aircraft in May-2013 and its ninth aircraft in Jul-2013, providing capacity to launch Jakarta-Singapore and potentially more domestic routes that were previously operated by Batavia. Both these aircraft and its current fleet of seven A320s were sourced from Tiger. Mandala tells CAPA that it is now looking to lease three additional A320s for delivery by the end of 3Q2013. Mandala initially planned to expand its fleet to 10 aircraft by the end of 2012, meeting an Indonesian requirement for airlines to have at least 10 aircraft within their first year of operations. But Mandala was able to postpone meeting this requirement as it struggled to secure slots at Jakarta. Mandala focused over the first 10 months on expanding outside Jakarta, launching routes from several secondary cities in Indonesia to Singapore, where it can leverage Tiger’s main hub. But its initial inability to operate out of Jakarta except during off peak hours resulted in a very low aircraft utilisation, contributing to initial losses. See related articles:- Tiger returns to profitability but faces challenges in Australia, Indonesia and the Philippines

- Tiger’s Indonesian affiliate Mandala starts to pursue faster expansion but faces tall order

Mandala works on distribution improvements

Mandala was already close to Batavia and had been working on implementing a codeshare with the carrier which would have significantly improved Mandala’s domestic network and its distribution as Batavia had a strong network of travel agents. Mandala is now working on establishing a link with Batavia’s agents. In its first nine months of operations, over 80% of Mandala’s sales came through direct bookings. It also only accepted credit card payments. Both posed huge limitations for Mandala as a large portion of Indonesian domestic passengers still use local agents and do not have credit cards. The latter is being resolved by signing up partnerships with ATM suppliers and convenience stores. Batavia’s network of agents and slots at Jakarta was also the main attraction to AirAsia Group, which forged an agreement in Jul-2012 to acquire Batavia. AirAsia dropped the deal in Oct-2012 following the due diligence phase and Batavia ended up in bankruptcy just three months later. See related article: AirAsia faces uphill battle in Indonesian domestic market after dropping plans to acquire Batavia

Batavia’s network of agents and slots at Jakarta was also the main attraction to AirAsia Group, which forged an agreement in Jul-2012 to acquire Batavia. AirAsia dropped the deal in Oct-2012 following the due diligence phase and Batavia ended up in bankruptcy just three months later. See related article: AirAsia faces uphill battle in Indonesian domestic market after dropping plans to acquire BataviaIndonesia AirAsia loses out on opportunity to take over Batavia routes

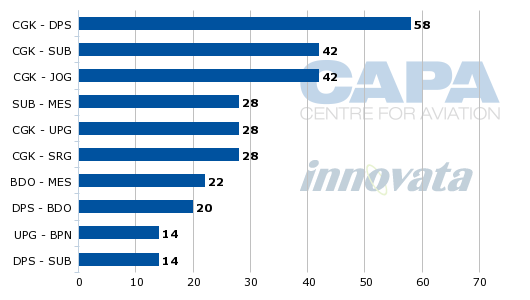

Somewhat surprisingly Indonesia AirAsia has not moved to take over any routes from Batavia. This is likely partly because AirAsia did not have the spare capacity in its fleet to immediately move onto Batavia routes. There may also have been a hesitation to fly Batavia passengers for free, which was a requirement for taking over Batavia’s routes and slots. Indonesia AirAsia’s failure to take over Batavia routes could put it in a weaker position in Jakarta compared to Mandala and Citilink, which have been able to secure additional valuable slots in exchange for taking Batavia’s passengers and routes. Indonesia AirAsia currently operates 22 A320s and does not have any additional aircraft slated for delivery in 1Q2013, which limited its ability to pounce immediately on the void left by Batavia. But the carrier’s 2013 fleet plan includes the delivery of eight A320s over the last three quarters of the year, giving it a year-end fleet of 30 aircraft. Indonesia AirAsia was already planning to allocate most its additional capacity in 2013 to the domestic market, a strategy that becomes more logical now that Batavia has exited. As CAPA reported on 05-Mar-2013:While Indonesia AirAsia is the largest carrier in Indonesia’s international market, it currently has less than a 5% share of domestic capacity. Most of the eight A320s being added by Indonesia AirAsia in 2013 will be allocated to the domestic market. The 2013 push for Indonesia AirAsia (IAA) began on 01-Mar-2013 with the opening of a new hub at Makassar, where the carrier has launched five new domestic routes. Makassar is the furthest point east in Indonesia served by Indonesia AirAsia, which previously only served the western half of the massive country. The carrier will continue to extend its network eastward in 2013 as it looks to develop a more meaningful network, which currently only consists of 12 domestic destinations. In an attempt to reach a larger demographic, Indonesia AirAsia (IAA) recently strengthened its distribution channels. The carrier now has a network of 3,500 agents, enabling it to access more of Indonesia’s massive population. A large agent network is Lion’s key strength and is necessary to compete in Indonesia’s LCC sector as most of the population does not yet buy tickets on the internet or have credit cards. Prior attempts by AirAsia to compete against Lion in Indonesia’s domestic market failed as AirAsia did not recognise the importance of offline distribution. AirAsia still faces an uphill battle domestically in Indonesia but is willing to invest heavily in trying to secure a large slice of Indonesia’s domestic market. The recent bankruptcy of Batavia, a full-service carrier AirAsia looked at acquiring in 2012, is a boost as it means there is one less competitor to worry about.See related article: AirAsia 2013 outlook marred by intensifying competition and continued losses at new affiliates Indonesia AirAsia reported passenger traffic of 5.8 million in 2012, a 17% increase over 2011 levels. But the AirAsia Group, which owns 49% of Indonesia AirAsia, does not break down domestic and international figures. Indonesia AirAsia has until now been primarily an international carrier and currently 57% of its seats and 68% of its ASKs are allocated to the international market, according to Innovata data. The carrier currently only has three domestic routes which are served with more than two daily return flights. Indonesia AirAsia top 10 domestic routes ranked on weekly frequencies: 11-Mar-2013 to 17-Mar-2013

Source: CAPA – Centre for Aviation & Innovata

Source: CAPA – Centre for Aviation & Innovata Growth in the international market continues to be slower than domestic

Indonesia AirAsia currently has less than 80,000 weekly seats in the domestic market, according to Innovata data. But it is Indonesia’s largest international carrier with over 100,000 weekly international seats to eight destinations. Most of its international capacity is allocated to Kuala Lumpur and Singapore, which it serves from several destinations in Indonesia. Indonesia’s international market remains relatively small and all of the country’s carriers are now focusing primarily on responding to rapidly increasing domestic demand. Indonesian carriers transported only 9.2 million international passengers in 2012, representing a 13% increase over 2011 levels. Foreign carriers also transported seven million passengers to and from Indonesia in 2012, according to preliminary DGAC data. Indonesian carriers annual international traffic (millions of passengers carried): 2005 to 2012 Note: 2012 figure is preliminary Source: CAPA - Centre for Aviation; Indonesia’s DGAC

Note: 2012 figure is preliminary Source: CAPA - Centre for Aviation; Indonesia’s DGAC Indonesia presents huge opportunities but profits may prove elusive

Given the huge opportunities in the domestic market it is hard to fault Indonesian carriers for focusing expansion close to home. The country’s booming economy, growing middle class and archipelago geography provide ideal ingredients for rapid domestic growth. But Indonesia’s domestic market is also intensely competitive and will become even more so in 2013 despite the exit of one of the country’s main carriers. The budget end of the market is particularly growing rapidly, with Mandala, Indonesia AirAsia and Citilink all attempting to significantly increase their market shares. The domestic capacity these carriers are adding in 2013 is just a small fraction of what Batavia provided prior to its bankruptcy. Market leaders Garuda and Lion also continue to expand rapidly, with Lion focusing growth at regional subsidiary Wings and new full-service subsidiary Batik. Sriwijaya, Indonesia’s third largest carrier, also is pursuing rapid growth in 2013 along with the launch of new full-service subsidiary Nam Air. See related article: Sriwijaya attempts to maintain its position as Indonesia's third largest airline as market explodes There is also rapid growth among Indonesia’s smaller carriers, particularly at Express Air, Sky Aviation and Indonesia Air Transport. Indonesia remains a highly fragmented market with about 15 carriers operating jet aircraft on scheduled services. While over-capacity could result on some routes, the demand curve is growing so fast the additional capacity should be absorbed in the near to medium term. The bigger concern is profitability as Indonesia’s industry has generally been in the red or just slightly in the black over the last several years. Given that the already tough competition will intensify further in 2013, it will be challenging for at least some carriers to grow successfully and chart a path to sustained profitability. https://centreforaviation.comCek berita, artikel, dan konten yang lain di Google News