How the world’s fourth-most-populous country is weathering the emerging-market turmoil

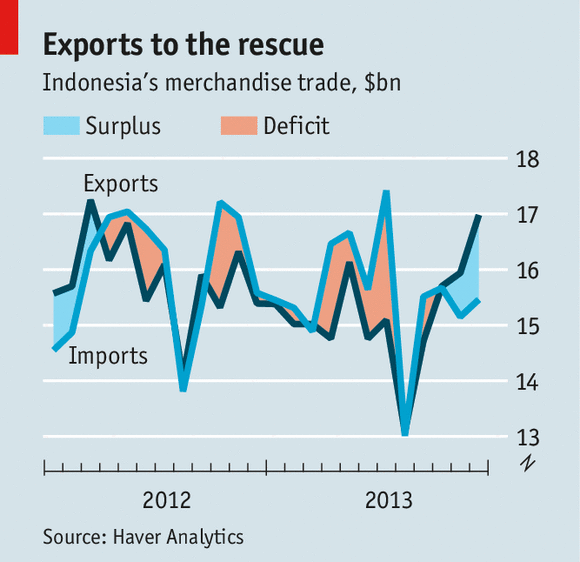

LAST year Indonesia was struck by the financial storm that pummelled emerging markets, earning itself a place among the so-called “fragile five” of the developing world. When in May the Federal Reserve began discussing plans to scale back its asset purchases, the prospect of higher yields in rich countries made investors reluctant to pour more money into emerging economies. Indonesia’s currency sank in value, along with those of other countries that had been prime destinations for rich-world cash. This year other emerging markets suffered a similar slump, caused by the Fed’s decision to go ahead with the mooted “taper”. Central banks in Turkey, India and South Africa have all hiked interest rates to defend their battered currencies. Yet Indonesia’s rupiah has rallied by 3.3% against the dollar—the most among major emerging-market currencies. Jakarta’s main stockmarket is trading close to four-month highs. And foreign funds have bought $1 billion more local bonds and shares this year than they have sold.

https://www.economist.com/

Cek berita, artikel, dan konten yang lain di Google News